Going live should not be the first time you discover how your strategy behaves. A trading rule can look reasonable in theory and still fail under a different date range, a different balance, or a different market regime. Gimmer’s current backtest workflow is built to reduce that guesswork by giving you a clear place to simulate a strategy, review the output, and iterate before you let the bot touch a live account.

Why Backtesting Still Matters

Backtesting is not a promise that a strategy will perform the same way in the future. It is a structured way to answer a simpler question: does this logic behave the way I think it does when it is exposed to historical market data?

That distinction matters. The point is not to treat a historical report like a guarantee. The point is to catch bad assumptions early, compare versions of the same strategy, and decide whether the setup is coherent enough to keep refining.

Where The Workflow Lives In Gimmer

Gimmer exposes backtesting in the places where it is most useful during strategy work.

- From an existing strategy card, you can open a backtest flow directly.

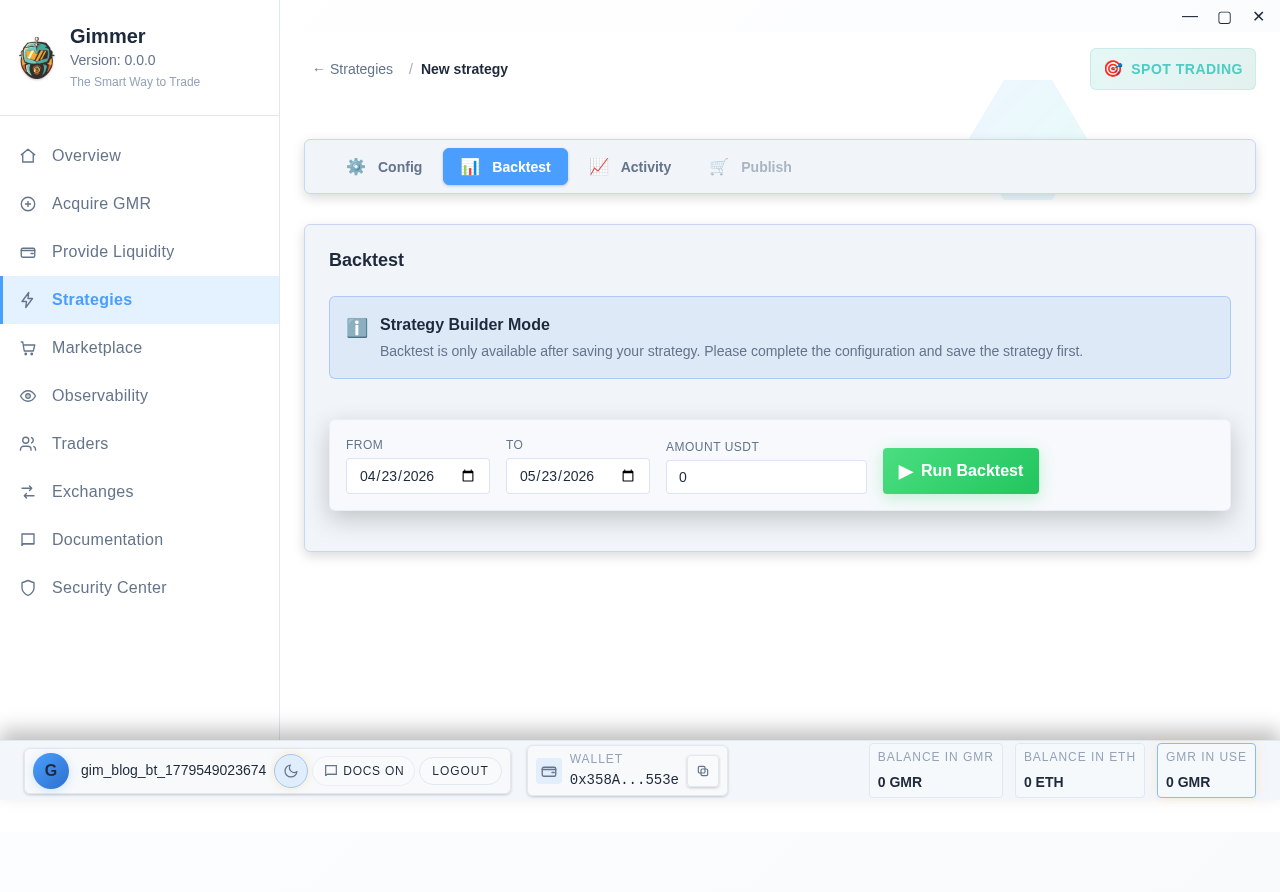

- Inside the strategy builder, the Backtest tab becomes part of the normal lifecycle once the strategy has been saved.

- For marketplace discovery, Gimmer also supports preview-mode backtests so users can inspect a strategy before committing to it.

That matters because validation is not treated as an afterthought. It sits close to configuration, activity review, and publication instead of living in a separate disconnected tool.

Start With A Test Window You Can Explain

The current backtest runner keeps the setup simple: choose a date range, set the amount you want to simulate, and run the test. That sounds basic, but it forces discipline. If you cannot explain why you picked the date range or the starting capital, the report at the end will be hard to trust.

A practical first pass is usually narrower than people expect. Test a period you actually want to learn from. Compare a trending stretch with a choppier one. Use a balance size that resembles how you would operate in reality instead of treating the backtest like a fantasy account.

Watch The Run Instead Of Waiting Blindly

One of the useful details in Gimmer’s current implementation is that the backtest flow is not just a submit button followed by silence. The runner tracks status changes as the job moves through the pipeline, including preparation, market-data fetch, import progress, processing, completion, failure, and cancellation.

That kind of visibility is operationally useful. If a run is still importing data, that is different from a strategy that already failed validation. If you decide the parameters are wrong, the workflow also supports cancellation instead of forcing you to wait for a run you no longer care about.

Review More Than Profit And Loss

The easiest way to misuse a backtest is to scan the final profit number and stop reading. Gimmer’s backtest workflow goes further than that. The result surface is built to help you inspect how the strategy behaved, not just whether the line ended higher.

Depending on the run, the review flow can include:

- Historical chart points for the tested run

- Report tabs and position data for deeper inspection

- Open and closed trade history

- Win/loss counts and other summary metrics

- Risk-sensitive signals such as drawdown, volatility, and profit factor

This is where a backtest becomes useful as a design tool. A strategy with attractive top-line returns can still be too unstable, too sparse, or too dependent on one narrow market phase. Looking at the report structure helps you decide whether the logic is robust enough to keep.

Keep The Comparison Loop Tight

Iteration is where the workflow becomes practical. Gimmer keeps backtest history for saved strategies, and the current backtest tab can reopen historical runs and apply saved settings back to the current strategy version. That makes it easier to compare what changed between one revision and the next instead of rebuilding the setup from scratch every time.

In practice, that means you can work in a tighter loop:

- Save the strategy.

- Run the backtest on a defined window.

- Inspect the output instead of guessing.

- Adjust the rules, sizing, or timeframe.

- Run the next version and compare.

That is a much healthier process than moving straight from a new idea to live execution.

What A Good Backtest Is Actually For

A good backtest does not tell you that risk has disappeared. It tells you whether the strategy logic is understandable, testable, and consistent enough to deserve another round of refinement. That is a lower-key promise, but it is the honest one.

Used that way, backtesting becomes less about hunting for a perfect equity curve and more about building a review habit. You are checking whether the strategy behaves coherently before the stakes become real.

Final Thoughts

Gimmer’s current backtest workflow gives strategy builders a practical validation loop: define the setup, run it against historical data, watch the live run state, inspect the report, and reuse what you learned in the next version. That does not remove market risk, but it does replace some avoidable uncertainty with a more disciplined process.

Want a clearer way to validate strategy logic before you go live? Download Gimmer and use the backtest workflow to review your setup before it reaches a real market.

— The Gimmer Team